It has been a while since I have written a financial planning article but I felt the need to write about refinancing today.

Many, if not most of you, may already know this, but it is important for those of you who don’t – right now is an incredible time to refinance your home. The mortgage rates and refinance rates are at historic lows in America.

My husband and I refinanced last summer and then just did it again in February because the rates had continued to go down. They dropped so much that we decided it was worthwhile to refinance again. We were originally with a 30 year at 3.95%, refinanced to a 15 year 2.875% in June of 2020 and just got an unbelievable 15 year at 1.99%. (I debated giving our actual numbers because I don’t think that you can still get 1.99% for a 15 year. Do NOT expect this low a rate. We were extremely lucky.)

(It is worth noting that I rarely recommend a 15 year mortgage. The flexibility of having a lower payment with a 30 year makes a lot of sense AND the difference between the 15 and 30 year rates are not that different right now. You can ALWAYS pay more if you want but it is nice to have that option.)

If you haven’t already, it is worth looking into what you can qualify for with a refinance. With the current low rates, you could:

- Decrease your payment to have additional cash each month for other needs

- Pay off other higher interest rate debt (credit card, student loans, car loans, etc.)

- Pull out some extra cash for home renovation projects or other worthwhile needs

- Keep paying what you were paying but with the benefit of a lower interest rate you will be done with your loan sooner. (This is what my husband and I are doing.) This also provides the flexibility of paying less if you need to in the future.

I will be honest with you, doing a refinance is a bit of a pain in the neck. You have to gather a list of paperwork and needed items. So the more organized you are the better. For us, everything was electronic so having a scanner was helpful too.

There are choices and decisions to be made, such as:

- Do you want to pull cash out? If so, how much cash do you want? To explain, if your home is worth more than what you owe on the mortgage you may be able to increase the loan amount and “pull cash out” for other things. At such low interest rates, this may make sense.

- What term do you want (15 years, 20 years, or 30 years)?

- Do you want to roll the closing costs into the refinance?

It does help to have cash available to “float” the change in escrow for property taxes and insurance but this is not necessary.

Your home is one of your biggest purchases and investments. It is worth looking into refinancing.

Some people go to a lot of time and effort using coupons and searching for the best deal on smaller ticket items to save money, yet they do not think about refinancing their home because it is not on their radar. Saving money on your mortgage is of a much larger magnitude.

I felt the need to send this article because by taking the time (hopefully between 4-8 hours) you could save yourself possibly tens of thousands of dollars depending on your current rate and how much you owe on your home.

I debated showing an example with numbers, but decided not to. If you are considering refinancing you should talk to a mortgage broker. Have them run some numbers for you so you can see for yourself what it could mean in your specific situation.

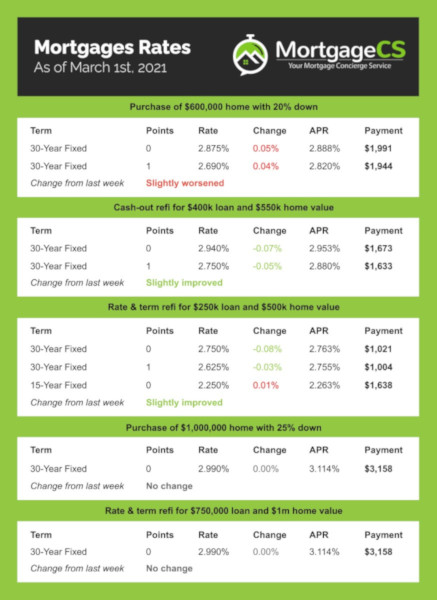

You can start with your current mortgage lender, your bank or contact me, I have a wonderful mortgage broker (mortgagecs.com) that I think the world of.

Feel free to contact me if you have any questions. I would love to help.

Recent Comments